You’re standing in a wet living room, your phone is already out, and you’re wondering whether any of this is covered. That moment of uncertainty is something we see constantly across San Diego County. The short answer is: it depends on how the water got in, and the distinction matters more than most people realize.

The rule your policy runs on: “sudden and accidental” vs. “gradual”

Every standard homeowners insurance policy in California is built around a single concept. If water damage was sudden and accidental, it’s almost certainly covered. If it was gradual, meaning it developed slowly over days, weeks, or months, your insurer will likely deny the claim.

A pipe that bursts overnight and floods your hallway before you wake up? That’s sudden and accidental. A slow drip behind your kitchen wall that’s been rotting the subfloor for six months? That’s gradual, and most policies treat it as a maintenance failure on your part, not a covered loss.

The reason insurers draw this line is simple: gradual leaks are discoverable. A homeowner who inspects their property reasonably should catch a slow drip before it becomes a five-figure problem. Sudden events, by definition, can’t be anticipated or prevented.

Where this gets complicated is the middle ground. Say a supply line to your washing machine has a small defect that finally gives way on a Sunday afternoon. The damage happened fast, but did the defect exist for a long time? Your adjuster may ask exactly that. The better your documentation, the better your position.

What’s typically covered (and what to expect from your adjuster)

Most standard HO-3 policies cover water damage restoration resulting from:

- A burst or frozen pipe (common in older Oceanside and El Cajon homes that weren’t built for rare cold snaps)

- A sudden appliance failure, like a washing machine hose that pops loose or a dishwasher supply line that ruptures

- A water heater that fails and releases its tank all at once

- Accidental overflow from a bathtub or sink

- Sudden roof damage from a fallen tree or windstorm that lets rain in

Your adjuster will look for evidence that the damage was acute, not chronic. Healthy, intact materials that got wet fast look different from materials that have been wet for a long time. Restoration techs using moisture meters and thermal cameras can usually tell the difference, and so can an experienced adjuster.

One thing worth knowing: most policies cover the water damage to your structure and belongings, but they don’t pay for the appliance or pipe that failed. If a dishwasher hose blows and floods your kitchen, insurance typically covers drying out the floors and cabinets. It won’t buy you a new dishwasher. Keep that in mind when you’re tallying up costs. For a realistic sense of what water damage restoration cost looks like in San Diego, including what insurance tends to pay and what falls to you, that breakdown is worth reading before you file.

Flooding is a separate conversation entirely

This is the single most misunderstood part of homeowners insurance, and in San Diego it matters a lot. Standard homeowners policies do not cover flooding. At all.

Flooding, in insurance terms, means water that enters your home from the ground up, driven by rising water. That includes storm surge, overflowing creeks and rivers, and the kind of sheet flooding that happens when an atmospheric-river storm hits and the ground can’t absorb it fast enough.

San Diego’s clay soils, especially inland from Chula Vista through El Cajon and into La Mesa, don’t drain well. When the county gets a hard rain after a dry stretch, runoff moves fast. If that water enters your home through a door, a garage, or a foundation crack, a standard policy won’t touch it.

Flood insurance is purchased separately, usually through FEMA’s National Flood Insurance Program (NFIP) or a private insurer. If your property sits in a designated flood zone, your mortgage lender has likely required it. But many San Diego homeowners in lower-risk areas skip it, and some of them have learned that lesson the hard way during recent wet winters.

Storm damage restoration from a roof breach that lets rain in directly is typically covered under a standard policy, because that’s rain coming through a sudden structural failure, not ground-level flooding. The distinction is how the water entered. Always document the point of entry when you can.

Mold: the coverage that shrinks when you need it most

Most homeowners policies include some mold coverage, but it often comes with a sublimit, a cap that’s far lower than the rest of your dwelling coverage. Sublimits of $5,000 or $10,000 are common, and mold remediation in a San Diego home with water trapped behind stucco walls or under a slab can run well past that.

The other catch is causation. If your insurer determines that the mold resulted from a gradual leak they don’t cover, they’ll also deny the mold claim. Mold that grows from a covered sudden event is a different story, but you need the underlying claim to hold up first.

San Diego’s marine-layer humidity makes mold a faster-moving problem than in drier climates. Mold can take hold within 24 to 48 hours of water exposure, and in a poorly ventilated coastal home, it can spread further into framing and drywall before anyone notices. Acting fast on any water event, covered or not, limits how bad the mold problem gets and preserves your options with the insurer.

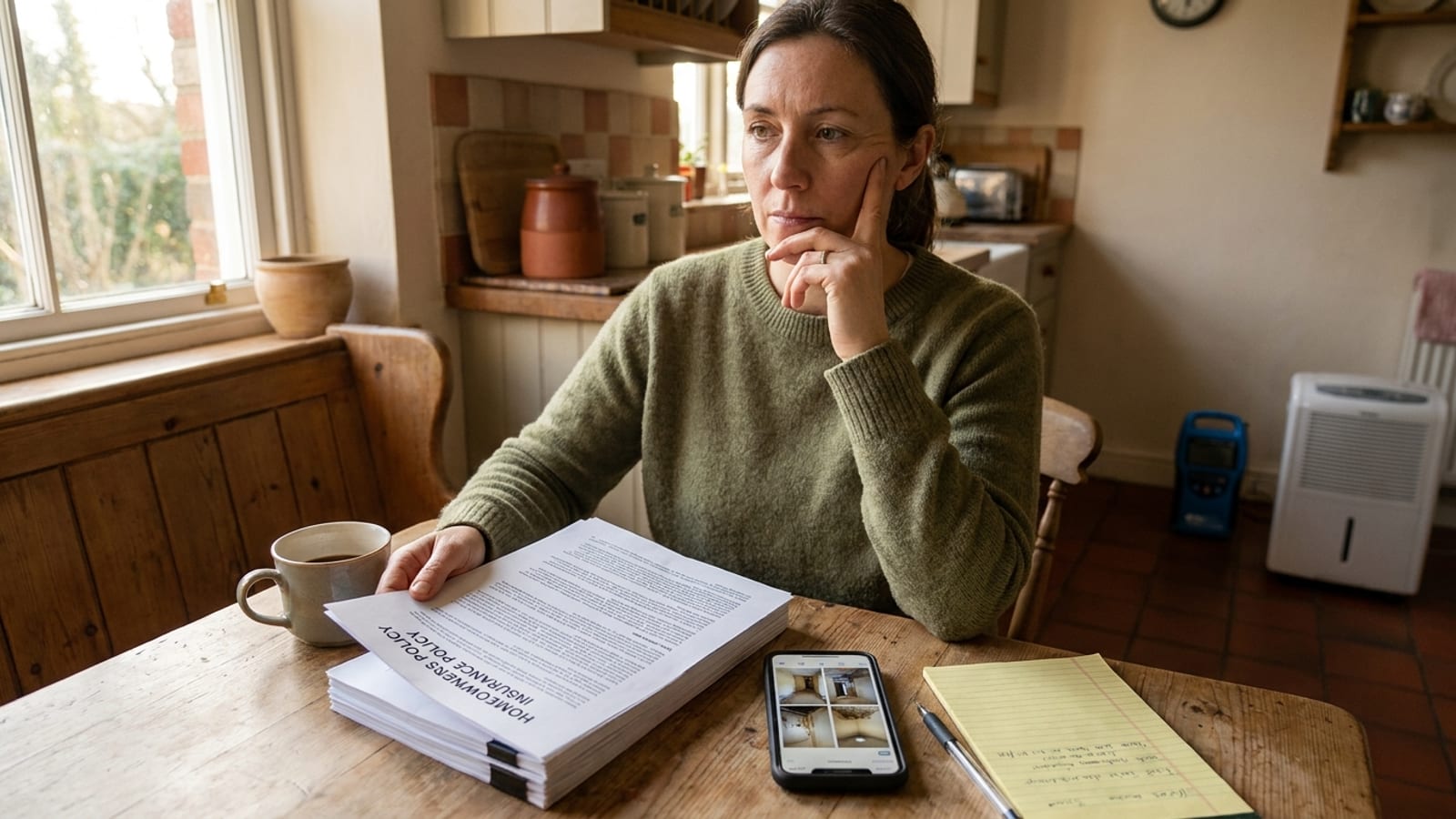

What to document before you touch anything

Good documentation is how you protect your claim from being reduced or denied. Before you start cleaning up or moving belongings, take a few minutes to do this:

Photograph and video everything. Capture the source of the water, the affected rooms, the standing water depth if visible, and any damaged belongings. Do this before extraction starts.

Note the timeline. Write down (or voice-memo on your phone) when you first noticed the problem, what you did, and when you called for help. Insurers look at response time. Acting fast and calling professionals promptly works in your favor.

Save damaged materials. Don’t throw away cut drywall, ruined flooring, or failed appliance parts until your adjuster has seen them or you have photos. Physical evidence supports the “sudden and accidental” story.

Get a written scope from your restoration company. A professional moisture assessment with documented readings gives your adjuster a clear picture of the extent of damage. The water damage insurance claim process goes smoother when you show up with organized documentation rather than a phone full of blurry photos.

One practical note: most insurers want you to mitigate promptly to prevent secondary damage. Waiting for an adjuster to arrive before starting water extraction can actually work against you if that delay lets mold set in. Calling a restoration company right away and documenting everything before they begin is the right sequence.

The “gradual leak” gray zone and how to navigate it

Sometimes damage doesn’t fit cleanly into either bucket. A supply line might have had a pinhole leak for a couple of weeks before it finally let go with force. A roof flashing might have been imperfect for years but only started leaking during a particularly hard atmospheric-river storm.

In these cases, the outcome often comes down to what the physical evidence shows and how the claim is presented. If materials show signs of long-term moisture exposure, staining patterns, deterioration behind walls, that history will be visible to an adjuster and to a restoration crew doing moisture mapping.

Being honest with your insurer about what you know matters. Trying to frame a gradual leak as sudden and accidental creates liability for you. If the claim is complicated, it can help to have your restoration contractor walk through the findings with the adjuster, since they speak the same technical language and can explain what moisture readings and material damage patterns actually indicate.

When to call us

Water damage is one situation where acting in the first few hours genuinely changes the outcome, for your home and for your claim. If you’re dealing with active water damage, call a restoration team before you have the insurance conversation fully sorted. The coverage question matters, but stopping the damage matters more.

We work with homeowners across San Diego County through the full process, from emergency extraction to final documentation for your insurer.

Call us at (858) 925-5546 for a same-day estimate.